By Satoshi Ikeda, Chief Sustainability Officer, Financial Services Agency, Japan

In this post for the Sustainable Finance Leadership series, Satoshi Ikeda sets out the reasons why Japan is leading the way in terms of businesses committing to reporting using the recommendations of the Task Force for Climate-related Financial Disclosures (TCFD).

2019 marked a major shift in the way Japan addressed the challenge of the climate emergency. One significant development was the rapid increase in the number of Japanese firms committed to reporting their approach to climate change using the recommendations of the TCFD, growing from 44 to 223 by the end of the year. As a result, Japanese companies are the largest group of TCFD supporters worldwide, making up almost one quarter of the total (see Figure 1). Furthermore, 23 per cent of Japanese TCFD-supporting companies disclosed the results of their climate-related scenario analysis during 2019, which far exceeds the global average of 9 per cent, as identified by the TCFD 2019 status report.

Figure 1. Number of TCFD supporters (end December 2019) (Source: www.fsb-tcfd.org/tcfd-supporters/)

Number of TCFD supporters (end December 2019)

One factor that helps explain this surge in commitment was the formation in May 2019 of a new public–private partnership, the Japan TCFD Consortium. The Consortium brings together institutional investors, financial institutions and business corporations in Japan to promote constructive dialogues around climate-related financial disclosures. Backing from Japan’s Ministry for Economy, Trade and Industry (METI), the Ministry of the Environment and the Financial Services Agency of Japan was instrumental in establishing the Consortium. Indeed, Japan’s long-term strategy for implementing the Paris Agreement centres on TCFD implementation as a way of promoting green finance to drive much-needed strategic action and industrial innovations for a low- and zero-carbon economy.

For Japan’s business sector and policymakers, the importance attached to TCFD implementation rests on four pillars

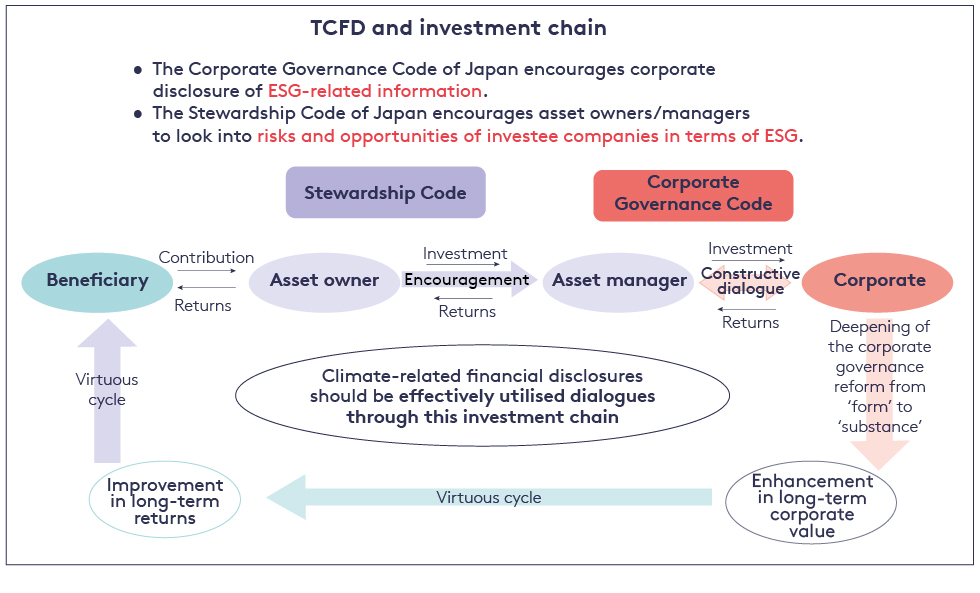

1. The TCFD can deploy capital markets to help rectify the market failures of climate change.

The TCFD is primarily a set of recommendations for climate-related financial disclosures. Yet, when it is implemented strategically along the investment chain, it can become a framework of constructive dialogue between business corporations and institutional investors, as well as other financial institutions. This dialogue can induce corporates to more thoroughly assess the financial impacts of physical risks and transition risks, as well as the opportunities resulting from climate change. The TCFD can thereby establish a mechanism for providing real financial incentives (such as the reduction in the cost of capital) for positive actions by business.

Economics 101 typically frames climate change as the problem of externalities, where market-priced transactions fail to reflect the true costs of carbon emissions. The creative use of the TCFD can help to correct these externalities to some degree by rewarding companies that align their business models with the Paris Agreement. This is the case because institutional investors and financial institutions are incentivised to preserve the long-term corporate value of their investee/borrower companies in the face of the climate emergency, and so are increasingly urging businesses to articulate the channels of climate change impact on their financial performances and effectively internalise externalities in their business decision-making.

Figure 2. TCFD and investment chain (Source: Author)

2. The TCFD enables a more granular approach to tackling climate change than carbon pricing alone.

A narrow view of climate-related challenges can lead to carbon pricing being promoted as the only tool to internalise externalities. However, carbon pricing is only one of many policy options that can be used to drive the transformation of markets; other options include product and emission standards, as well as investment in innovation and infrastructure. Constructive engagement around TCFD-aligned disclosures enables companies and investors to focus on every aspect of the transition process in a decentralised way. As such, the carbon footprints of a company can be assessed in a more focused way (e.g. in terms of a differentiation of Scope 1, 2 and 3 emissions) and actions by institutional investors and financial institutions can be taken accordingly. More importantly, in such settings, the potential of opportunities that a particular company possesses can be more easily factored into the corporate valuation of the company. As a result, the TCFD framework can powerfully complement carbon pricing systems.

3. The TCFD takes an inclusive approach to driving all industrial sectors towards the transition to net zero emissions.

Climate finance must catalyse and support each and every company so that they all make the transition from brown to green. The TCFD allows diverse approaches to be taken by corporates in tackling climate change. What is missing, however, is a set of principles to guide businesses in setting proper targets and metrics (i.e., key performance indicators – KPIs) for a transition that is fully aligned with the Paris climate goals, and to assist institutional investors and financial institutions in monitoring their progress. This is why I believe that the development of guiding principles for climate transition finance is critically important. In my view, this should be the next task for the TCFD or alternatively, should be developed by members of the International Capital Market Association (ICMA), which has pioneered the Green Bond Principles.

4. The TCFD can help trigger the breakthrough innovations that will be vital for achieving net zero emissions by 2050.[1]

Embracing the TCFD framework provides a strong impetus for boards and executives to deepen their strategic thinking and organisational learning around climate change. Combined with scenario analysis exercises, CEOs cannot escape telling a sense-making story of how their company will survive and enhance corporate value in the face of climate change. This sense-making story will offer justification and create psychological safety for corporate employees striving – with inevitable trial and error – to develop low- and zero-carbon innovations. In other words, such a sense-making story that sounds plausible to employees will stimulate the process of ‘exploration’ (i.e. the pursuit of new knowledge) and facilitate new combinations of ideas (i.e. innovations) within a company. If this would happen in every industrial sector, it would be a very positive precursor to a decarbonised world.

The TCFD – a framework for strategic change and innovation

It is clear that the TCFD is far more than a set of reporting guidelines. In fact, Japan’s business and policy communities have embraced the TCFD as a framework for strategic change and innovation. Japan hosted a global TCFD Summit in October 2019 to promote dialogue on realising this potential and plans to host a second TCFD summit later this year.

In this critical year for climate finance, the TCFD will take a central role in driving corporate actions towards a low- and zero-carbon economy by facilitating constructive dialogues between institutional investors/financial institutions and business corporations. The end result should be active collaboration between business and finance on setting appropriate KPIs for climate transition. Thus, an important part of the path to the COP26 UN Conference will be to establish how best to use the TCFD implementation to bring about this collaboration and also to create an intergovernmental structure that will ensure the effective implementation of the TCFD framework globally.

[1] This paragraph is inspired by the idea of Dr. Akie Iriyama, Professor of Waseda Business School, Waseda University.

The views in this commentary are those of the author and do not necessarily represent those of the Grantham Research Institute.

Keep in touch with the Grantham Research Institute at LSE

Sign up to our newsletters and get the latest analysis, research, commentary and details of upcoming events.