Why the UK’s smart meter rollout needs to be smarter

Ahead of the Business, Energy and Industrial Strategy Select Committee’s session reviewing the management of the Smart Meter Implementation Programme, to be held on 9 January 2019, we publish the first of two commentaries on smart meters. Read the second, ‘Are smart meters good for UK households?’, here.

Smart meter technology is an important part of creating a more flexible – and potentially cleaner – energy system. By supplying crucial information into the system, these meters have considerable potential to reduce costs for households and suppliers, increase operational efficiency, and facilitate the integration of increasing flows of renewable energy into the grid, contributing to climate change objectives. So far, so good.

Based on these expected benefits, in 2013 the UK government released its ambitious Smart Meter Implementation Programme (SMIP), whose aim was to install smart meters in every UK home by 2020. While the sheer scale and complexity of the programme and the resultant risks have long been flagged, it was the release of a National Audit Office (NAO) report in November 2018 that really focused concerns about implementing the SMIP, creating a storm of media attention. The NAO report highlights escalating costs, problems with meter functionality – particularly the current supplier-specific technology (the first-generation ‘SMETS1’ meters), which is being phased out by October 2019 – and overall operation of the system.

Media scare tactics?

The media has been publishing negative stories about the SMIP since its inception, implicating energy suppliers and highlighting health and privacy risks that may render consumers wary. While some of these stories may hold a degree of legitimacy, many are based on scant evidence. For instance, concerns have been put forward with regard to radio waves from smart meters; however, levels are estimated to be well below those of mobile phones and a minute fraction of the level dictated in standard international guidelines.

The media’s often misrepresentative account of smart meters poses an issue for the SMIP, as the programme’s success ultimately hinges on convincing households to actively express interest in smart meters and facilitate their installation. Given the amount of conflicting information targeted at households, it is understandable that consumers are not queuing eagerly to invite installers into their homes.

Who wins, who pays and to what end?

According to the Government’s own cost-benefit analysis, the total benefits (not accounting for costs) of smart meters to the UK economy are estimated at approximately £16.7 billion between 2013 and 2030 (see Figure 1). Of this total, 32 per cent comes from energy cost savings that households will accrue directly, 49 per cent from supplier cost savings (which may or may not be passed on to households), and the remainder comprises carbon savings from increased renewable generation and system-level operational efficiency gains.

Figure 1: Estimated benefits of the Smart Meter Implementation Programme (2011 prices) Source: Department for Business, Energy & Industrial Strategy’s Smart meter roll-out (GB): cost-benefit analysis, 2016

The Government has had to make a number of assumptions in making these assessments, firstly regarding the savings that households will make after installing a smart meter, and secondly about the impact that smart meters will have on the future energy system. The as-yet unknowns include: how responsive households will be to real-time information on their consumption patterns; how much suppliers will really save from averted manual meter readings; how much renewable energy a smart system will accommodate; and how smart meters will help to facilitate and increase operational or technical innovation, such as effective time-of-use tariffs or the integration of electric vehicle batteries as a flexible demand response tool.

Engineering estimates may not always be spot-on; in fact they can be quite far from reality in some contexts. The point is that benefits could fall considerably short of – or exceed – expectations. Whether and in what direction they do depends in no small part on the success of the smart meter rollout and its impact on supplier and investor responses.

On the flip side, the Government estimates the total costs to be around £11 billion (Figure 2). This estimate – also rooted in assumptions – includes the costs of the meters, installation, and the communication hub system. In addition, householders may have concerns about data security and the inconvenience of having to commit half a weekday to overseeing installation – these costs may be less tangible but they are real costs for householders and should not be neglected when considering the causes of low take-up rates.

Figure 2: Estimated costs of the Smart Meter Implementation Programme (2011 prices) Source: Department for Business, Energy & Industrial Strategy’s Smart meter roll-out (GB): cost-benefit analysis, 2016

*Smart DCC was granted the licence to build and maintain the infrastructure that underpins the roll-out of smart meters across the UK

The net benefit to society – the difference between the total benefits and costs – is therefore around £5.7 billion, or £200 per household – although how much of that will accrue to households is unclear. It is also worrying that the £5.7 billion figure had already been revised down by £1 billion since the 2013 business case, and based on NAO estimates of mounting costs is likely to fall further still.

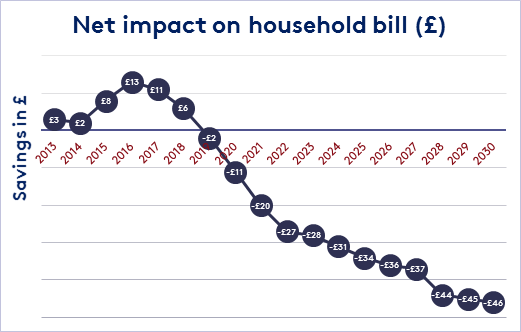

Based on the above benefits and costs, it is estimated that by 2030 households will be saving £46 per year on a duel fuel energy bill (Figure 3). However, much of the costs are upfront, while the benefits will accrue in the future. And a lot of uncertainty exists in these numbers.

Figure 3: Estimated net impact of smart metering on household bills (2011 prices) Source: National Audit Office: Rolling Out Smart Meters, 2018

Smarter consumer engagement

There is a risk of disengaging people by repeatedly and narrowly emphasising near-term household savings when many simply do not believe these will be realised – apparently with good reason, given the points we raise above.

Insisting such savings are possible without providing robust evidence creates the space for scaremongers to capitalise on evidentiary uncertainty. Once people choose a side, it is notoriously difficult to change minds and polarisation becomes increasingly likely (research has demonstrated this, for example, in the climate change ‘debate’ and in partisan politics).

Finally, let’s not forget that design and communication flaws in programme rollout have led to failures of promising environmental policies in the past (RIP the Green Deal). If the SMIP is to be successful, much more (rigorous) research needs to be undertaken to understand how to engage consumers. For instance, educating the public on the medium-term private and social benefits of a smarter energy system – for which smart meters are merely an enabling technology – may be a better way to facilitate public engagement.

What is clear is that the current strategy is not up to the task. The Government needs to get more creative with its talking points, diversify its messengers, and ultimately provide this important initiative with a real chance of transforming the UK’s energy system for the better.

Minor edits were made to this commentary on January 9 to clarify the estimated impacts of smart meters on household bills.

In 2019 Greer Gosnell and Daire McCoy will be conducting work that aims to understand the relative importance of various barriers to and drivers of smart meter adoption in the UK. This research is funded by Horizon 2020 ENABLE.EU and the ESRC Centre for Climate Change Economics and Policy (CCCEP)

The views in this commentary are those of the authors and not necessarily those of the Grantham Research Institute.